Top-Down Budgeting: Pros and Cons

Top-Down Budgeting: Pros and Cons

Neither approach inherently outshines the other, and specific corporate budgeting methods, such as driver-based budgeting, can be compatible with both paradigms. The key lies in comprehending your organization’s inner workings and seamlessly integrating your budgeting process with them. Equally important is grasping the advantages and drawbacks of each model before making a selection.

Top-Down Budgeting:

A top-down budgeting process commences at the senior management level. They take on the responsibility of formulating a budget that encompasses the entire organization, apportioning resources to various departments in accordance with overarching company strategies and annual organizational objectives. Historical performance and present market conditions inform this allocation, utilizing past budgets and performance metrics to decide each department’s allocation based on their historical contributions to company goals.

Departments then construct their budgets based on the allocated resources. Frequently, a portion of funds remains at the corporate level, permitting last-minute adjustments or additional resource requests if departments believe they lack what’s necessary to fulfill their specific goals.

Pros of Top-Down Budgeting:

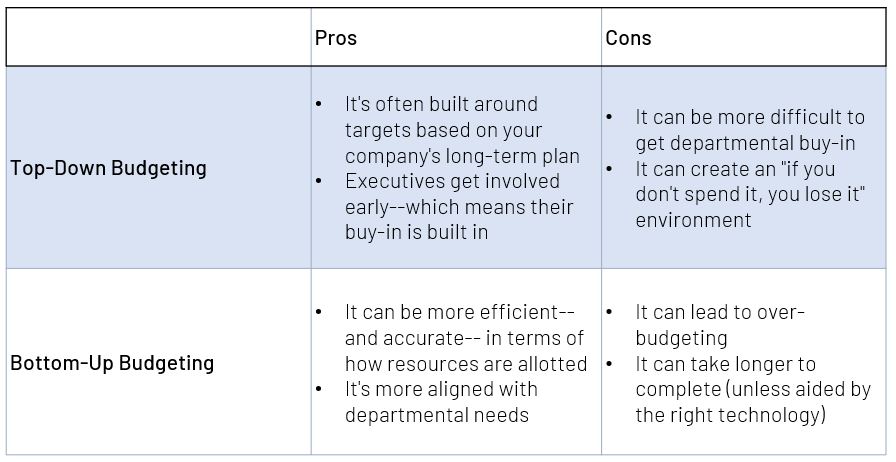

- Executive alignment is automatic, ensuring that the budget mirrors management’s perspective, goals, and the company’s future growth plans and strategic direction.

- By capping departmental budgets according to overarching objectives, departments become more accountable for reaching these goals.

- It can expedite the budgeting process while enhancing organizational transparency regarding company-wide expenditures.

Cons of Top-Down Budgeting:

- Securing departmental buy-in can be challenging since individual departments aren’t directly involved in the budgeting process.

- Intra-departmental conflicts may arise if one department perceives that their goals are being overshadowed in favor of another department’s objectives.

- It can foster a culture of “use it or lose it,” where departments feel compelled to spend all allocated resources, even if unnecessary, to avoid future budget cuts.

Bottom-Up Budgeting:

In contrast, bottom-up budgeting commences at the departmental level. Each department formulates budgets based on their projected requirements for the upcoming year, encompassing planned initiatives, ongoing programs, and staffing needs. To facilitate this process, company-wide objectives and expectations are typically communicated to departments beforehand, granting them a broader organizational perspective as they develop their plans and preventing isolated budget requests.

Departments present their budgets for evaluation, with the finance team or budget committee scrutinizing each item in relation to overarching organizational objectives. A comprehensive company budget emerges through this collaborative effort.

Pros of Bottom-Up Budgeting:

- It often operates more efficiently, as departmental teams have a sharper focus on their resource needs to achieve their goals.

- It aligns more closely with departmental requirements, as departments are ultimately responsible for their budgets.

- Managers and teams are more likely to support the overall results, as they have a deeper understanding of their individual programs and initiatives.

Cons of Bottom-Up Budgeting:

- There’s a risk of over-budgeting, as departments may inflate their requests to secure resources.

- Creating a bottom-up budget can be time-consuming and resource-intensive unless facilitated by suitable technology.

Determining the Right Approach for Your Business:

Choosing the most effective approach for your business hinges on understanding your organization’s operational psychology. Are teams more effective when they devise their own ideas, or do they prefer leadership to provide a clear plan of action? How adept is your organization at creating transparency in goals and strategies for swift resource reallocation?

In some cases, you may not need to choose one model over the other but instead blend both approaches to gain insight into departmental and organizational goals or meet specific objectives. You might implement a longer-term top-down plan and use a rolling or traditional bottom-up method for nearer-term planning. Alternatively, you may choose to go into more detail on cost structures for goods or services in some years, building a bottom-up budget from there, while taking the opposite approach in other years.

Ultimately, the objective of both top-down and bottom-up budgeting approaches remains the same: ensuring intelligent allocation of resources to support the overarching business strategy and goals. With this common focus, either model can thrive.